INSIGHTS

Common and not so common sustainability themes

How can companies and stakeholders easily identify those sustainability issues that are hot and those that are not? Fronesys offers a materiality hit parade.

How can companies and stakeholders easily identify those sustainability issues that are hot and those that are not? Fronesys offers a materiality hit parade.

The sustainability press today is filled with coverage of a wide range of non-economic issues and impacts that companies have to pay attention to. But which of these issues do companies believe to be material to their performance, and which are not?

To answer this question, Fronesys analysed sustainability reports from 31 different companies, as published in Materiality Futures, our coverage of where the art and science of materiality reporting has got to. In this report, authored by Chris Tuppen, we found that the 31 companies in our study referenced nearly 140 sustainability issues between them, covering economic, governance, environmental, social and global trends.

Before we examine the sustainability issues in question, we should lay out how we chose which companies to include in our analysis. Remember, the study was about materiality reporting, and so our goal was to identify all those companies that met the following criteria:

- they published a materiality matrix of the sort laid out AccountAbility’s Materiality Report, a methodology subsequently adopted as the basis of the related Global Reporting Initiative (GRI) technical protocol on report content.

- their materiality matrix had at least three degrees of granularity per axis ( the way most companies present their materiality matrix, the vertical axis usually represents the stakeholder, and the horizontal axis the company)

- individual issues are identified and positioned on the matrix

As a result of sifting through sustainability reports via corporateregister.com, Framework:CR materiality analysis, and internet search engines, we found only 31 companies actually met our criteria. Although many companies respond to GRI indicator 3.5 and say they use a materiality determination process, relatively few disclose much detail on either the process or the determined level of materiality for individual sustainability issues. Note that this analysis covers sustainability reports published before August 1, 2011. A full list of the 31 companies is available on the Fronesys website.

Although we could simply list the 140 or so issues that crop up via the reports of these 31 companies, we can understand their significance better if we explore some metrics:

- number of companies covering the issue

- average, minimum and maximum scores on the company axis

- average, minimum and maximum scores on the stakeholder axis

To prevent the analysis from being clouded by issues that are important to just one or two companies, we did a further sift to exclude issues that were not featured by at least five different companies, and found that 50 issues met this additional filter.

Hit parade

So which are the top sustainability issues?

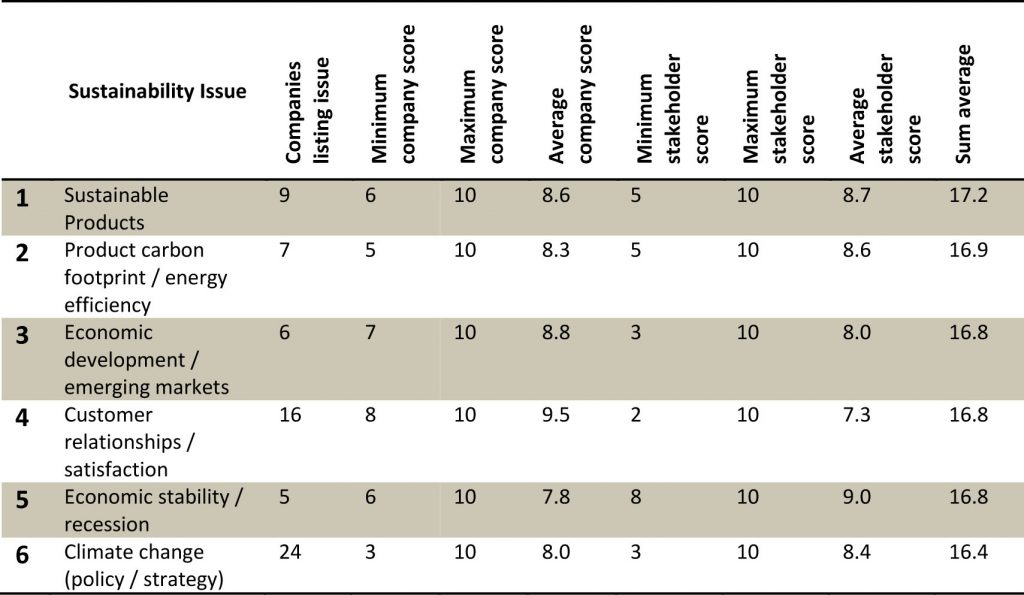

Here’s a table that lays out the top six sustainability issues, based on a sum of the average score from a company perspective and the average score from a stakeholder perspective:

Source: Fronesys Materiality Futures report, 2011

So if the top sustainability issues in company materiality reporting are sustainable products, carbon footprints, economic development / emerging markets, etc, etc, which are the ones that are bottom of the pile? Well, here’s the bottom six, using exactly the same methodology as above:

- Work/life balance

- economic contributions, including tax

- volunteering

- freedom of association

- biodiversity

- senior executive remuneration

It is not that these are unimportant issues. After all, biodiversity, for example, featured on the materiality matrix in 19 separate companies, the most commonly cited issue after climate change and diversity. Yet it is not rated highly as a material issue, either by companies or stakeholders. It is almost like they don’t know what to do with the issue – but that would be the topic of another blog altogether.

Overall, it is very useful to get a view of what issues are actually making their mark on corporate managers – one has to assume that the more public the statements about materiality get, the more companies need to act (and be seen to be acting) to manage these impacts.

Maintaining such a Top 50 list could be a useful service to the players in the market: companies can compare their own analyses with those of their peers, while stakeholders get a list of which issues are cooking and which need more attention.

Here’s to more material number-crunching.

MORE FROM INSIGHTS

Assessing the impacts and outcomes of integrated reporting

Fronesys founders played influential roles in the development of the integrated reporting movement, a corporate reporting mechanism that now has around two thousand listed companies as its adopters, and which is now part of the mainstream of corporate reporting. So, perhaps, now is as good a time as any for Jyoti Banerjee to look back and assess the outcomes and impacts, as well as the what-might-have-beens, of this new form of corporate reporting.

Integrated thinking is focus of chapter in new Oxford handbook

Oxford University Press has just released a new chapter from the forthcoming Oxford Handbook of Food, Water and Society: Integrating Multi-Capital Thinking in Business Decisions. The new chapter, contributed by Fronesys partner Jyoti Banerjee, explores how we need to change our understanding of value. Here is Jyoti’s account of what you can expect in this new publication.

A Shift in Perspective – How Universities Create Value

Jyoti Banerjee, partner at Fronesys, highlights that by adopting the principles of integrated thinking and reporting, universities can move away from a focus on reporting short term financial metrics to a multi-stakeholder approach which offers compelling narratives about their value.

SOCIAL FEED

[juicer name=”fronesys” per=’9′ pages=’1′]